This blog is mostly about recording and sharing ‘aha’ moments which i come across while studying various businesses in Indian stock market. This post is about things that i learned about Indian financial space accidentally while analyzing Edelweiss financial services.

Background:

Barring few exceptions, most consistent wealth creators in India are generally limited to 4 sectors: Information technology, Pharmaceuticals, Financials, and Consumer facing branded companies (2&3-wheelers, FMCG, housing-related etc.). However, IT and Pharma are going through their fair share of churn in their business models.

IT – I may be the 100th person 🙂 to tell you about the coming disruption of Social, Mobile, Analytics, Cloud (SMAC) to the business model of IT companies. Besides, top 3 sectors serviced by Indian IT companies are undergoing tremendous change and managements are struggling to adapt to them. For eg: Banks & Insurance companies are struggling due to negative interest rates & regulatory changes; Hardware IT companies like Dell, HP, Intel, Cisco are finding tough to match cloud services; retail companies like Macys, JCP, Belk, Target due to the E-Commerce onslaught from Amazon.

Pharma – It is not the FDA issues that am worried about. I strongly believe in, “what doesn’t kill you, will make you stronger”. FDA concerns will stregthen well-managed companies. But am worried about something else. Neelkanth Mishra of Credit Suisse pointed out in an interview: “Earlier, Pharma companies are valued for base business + one-off cashflows discounted back. However, now one-off bounties are included as regular cashflows and valued accordingly”. Besides there is no visibility for blockbuster drugs going off-patent beyond FY’18-19.

Hence, understanding financials is very important and you cant ignore the biggest wealth-creating segment. This blogpost is an on-going effort to learn the business model of financial institutions in India.

According to me, there are 4 broad themes playing out in financial services:

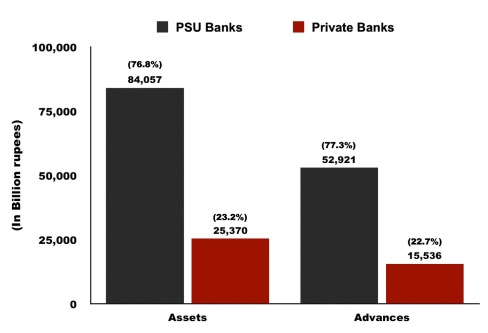

- PSU banks which control 70% of the credit are sitting ducks and one of the greatest value migration happening right in front of us.

- Technology and competition from new licensed players will disrupt both the payments space and retail savings part. We already saw record mobilization of funds by Bandhan Bank at higher interest rates.

- But risk pricing can’t be disintermediated by technology in my opinion. It is not the technology part that is harder. Human short-term greed is the problem. You need an fanatic manager who eschews short-term greed and pressure from PE players & truly focus on the long term vision of the business. Until that happens, you will hear stories like Lending Club, P2P scams in China etc. and people will develop mistrust about the platform.

- Over the long-term, net interest margins for Indian financial players could come down due to the technology and competition. Hence, am very vary to pay high price to book multiples.

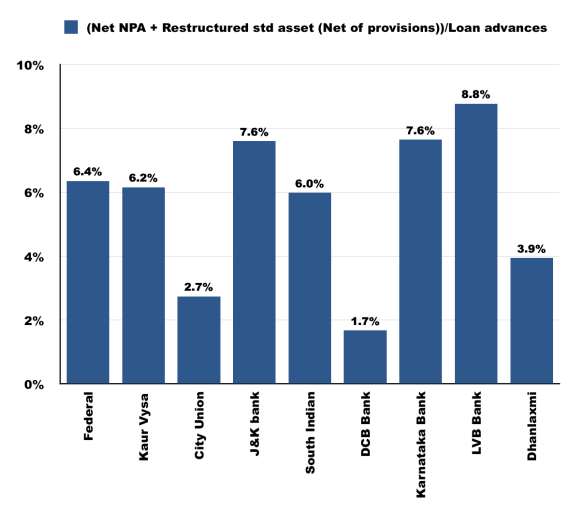

As I analyzed in earlier blogposts (Part-I & Part-II), most PSU banks, and old-age private banks are in deep troubles due to NPA. As a next step, I wanted to study about NBFCs. It can be largely divided into 5 groups:

- Retail loans like Auto, Gold, & Consumer loans – Bajaj, Shriram City, Shriram Transport, M&M financials, Sundaram, Chola finance, Muthoot finance, Manappuram, Capital first, Magma Fincorp.

- Housing finance companies – HDFC, GRUH, Repco, Canfin, Indiabulls, Dewan, LIC, GIC housing.

- Microfinance/Small finance banks – Ujjivan, Equitas, Satin, SKS, Arman Financial.

- Broking companies diversifying – Edelweiss, Motilal Oswal, IIFL holdings, JM financials.

- Industrial conglomerates building NBFCs – Religare, Reliance Capital, L&T financial, Piramal Enterprises, Aditya Birla financials.

As usual, I followed the process of exclusion to focus down the players i wanted to study. I believe there is some kind of frothiness in terms of future business expectation and valuation going on in housing finance & microfinance space. As management is the top filter to invest in leveraged business like financials, I avoided both broking companies (due to their involvement with NSEL scam) and Industrial conglomerates (for their poor corporate governance & capital allocation abilities except in the case of Piramal Enterprises). However, following passage from Forbes India intrigued me about the Edelweiss financial services.

Prudent risk management kept Edelweiss away from NSEL fiasco when other leading brokers like IIFL, Motilal etc. burnt their fingers & reputation. Hence, i wanted to dig deeper about the company.

Edelweiss Financial Services:

According to me, basic smell test for any company is ROE and growth >15%. It passed on both counts.

Business model:

Their quarterly presentation gives very good idea about their various business lines. It is present in both credit side (NBFC) and non-credit side (like Insurance, asset management, wealth management, Investment banking etc.).

My view:

It has got fairly good presence in wholesale credit segment, Asset reconstruction credit, Investment banking, Agri warehousing . However, their retail NBFC, Insurance, Wealth management segments are still in the investment phase and long way to go before contributing meaningfully. On the consolidated basis, only in Q1 FY’17 they crossed ROE of 15%. We have to look for the cosistency of ROE, ROA, and how various platforms are scaling up.

However, this post is not about the analysis of Edelweiss financial services. It is more about things i learned about the Indian financial space from its Investor day transcript. It was an excellent talk from the CEO Rashesh Shah. I made few edits for my understanding and grouped interesting parts of the talk into 3 segments and various sub-segments (I strongly recommend interested people to read the 32-page original transcript which is full of insights about the Indian financial space).

I. Overview of Indian credit market

II. About business model of financial institutions

III. About Edelweiss business lines

I. Overview of Indian credit market:

Three broad trends happening in the Indian credit market:

- Credit markets are getting segmented and new avenues opening up

- New avenues for capital/liabilities opening up

- From the risk management point of view, more data or information is available with info from credit bureaus and analytics

Bird’s eye view of Indian credit market:

Even today the total credit outstanding in the entire banking sector is about Rs. 75 lakh crore out of which about 52 is with the PSU banks and 22-23 is with the private sector banks. The total credit of all the non-banks put together is only Rs. 8 lakh crore only. So it is a smaller base and even within that there are the larger NBFCs who are mono lines focused on a particular segment. Out of Rs. eight lakh crore at least Rs. 4.5 to 5 lakh crore is housing finance. So the non-housing finance is only Rs. 3-4 lakh crore in the non-bank markets. So if you keep on slicing like that you can estimate that there is at least a fair amount of opportunities are still available.

Credit markets getting segmented & newer segments opening up:

Pre 2000 there was hardly any retail credit market in India. We had few housing loan products, and a few auto loan products but the retail credit as we all know now, it did not exist. For the first 8–10 years when ICICI Bank, HDFC Bank all of them started ramping up the retail credit part of the opportunity, it was still largely in the urban areas, largely in the metros and also largely to salaried employees of the companies. However, over the last 7-8 years, the credit market became very heterogeneous and there are smaller and smaller segments of credit which are starting to open up. Recent times, many NBFCs have seen good growth in segments like auto loans (2-wheeler, 3-wheeler, tractor, commercial vehicles – LCV/HCV) to rural markets, micro finance companies, SME Sectors, Self-employed where earnings are erratic and where there is no clear salary certificate etc. Also the credit bureau getting setup, and now with analytics you can have a fairly good estimate of cash flow. This is a completely new market, which has opened up.

Market is getting segmented which happens with every new entrant. So if you see consumer goods in India, there was one detergent out there. Then suddenly Nirma, Rin and Wheel and a lot of others came about. As the market is growing the segment doesn’t remain static. So like the SME segment itself has at least 8-9 categories from equipment finance to what is called UBL – unsecured business loans, to SME secured, to trade finance, to various other categories. And SME itself has got micro SME’S where the average loan size is about Rs. 8-10 lakhs, to SME’s where your average loan size is about Rs. 30-40 lakhs, to mid SME’s where your average loan size is a crore, to large SME’s where it can be up to Rs. 5 crore. And these are very very different categories – their needs, their banking experience, their track record, and the information available about them are very very different. So if you saw in housing also, companies like Repco, Gruh and all grew because they went after the self-employed segment, which was not there earlier. Until 8-9 years ago people were not actually going after that because of lack of enough underwriting data or the analytics or the credit bureau information. So now what is happening in credit is newer segments are opening up. For the newer players, a thousand, two thousand or five thousand crore rupees market segment is also exciting, while for an existing large player it may not be. And third is when you become large and if you have been doing a particular asset class it is very hard for organizations to change, especially for mono lines becoming multi line is very hard. If you see Bajaj Finance is not a monoline, they are now multiline. Their real growth started the day they removed auto finance from their name. It used to be called Bajaj Auto Finance, and then the day Auto was dropped is when the growth started happening. Going after the new emerging opportunities you should be able to go after multiple, smaller opportunities where you can learn the game. You have to be agile, have to be slightly more adaptable, which may be the new age firms are.

Bank Vs NBFC debate:

The pros about a bank is that you can choose your scalability because if there is a glass ceiling on NBFC at Rs. 100,000 crore and if you really want to think about the next 10– 15–20 years and at some point you want to be Rs. 2 lac–3 lac crore, then you need to think. It is currently hard to see an NBFC scaling up more than Rs. 100,000 crore but as I said it keeps on changing. 10 years ago I would have said Rs. 20,000 crore; 3–4 years ago I would have said Rs. 40,000 crore, now I am saying Rs. 100,000 crore is the glass ceiling for NBFCs. The other thing that the banking structure will allow you is some more stable regulatory environment because a non bank is always exposed to RBI changing its view on NBFCs and we have seen that happening over the years. The last 3 years RBI has been very positive about NBFCs but it can easily change if there is some chaos in the industry. So you are always suspect to scalability issues and the change in the regulatory environment if you are a non bank. On the other side what has happened is the profitability of the non-bank has improved as compared to banks. As I keep on saying, how many banks you can name who have RoE above 18% and how many non banks you can name who have RoE under 18%?

Liability side is getting broad based:

The biggest problem to be in the credit business is you need capital and it is not the asset side problem, it is the resource side. The liability side problem is bigger. It is very hard for a non-business group to build the resource side of the equation. The asset side work will always be there. What has changed in the last 3 years is the resources side has become lot more easier for NBFCs. Lot of the older firms was able to grow because they had access to bank relationships and other funding options. The bank credit as a percentage of their borrowing is starting to fall as the bond market is starting to develop. There are a lot of new players in that, for example insurance companies are becoming a big supplier of credit to the NBFCs. It was always earlier banks, and then mutual funds started after 2008-09 when they started getting some scale. But in the last three years insurance companies are emerging and I can guarantee you that in the next five years insurance companies are going to be big provider of capital, long-term capital to the NBFCs. An insurance company on a traditional policies will allocate 85-95% of the money in bonds and only 5-15% in the equities. So all that is starting to change and so I am saying that liability side change is very exciting. A lot of more NBFCs, which are not constrained by resources, are now starting to take advantage of.

II. About business model of financial institutions:

What can kill you in credit business?

But as with everything in credit, you have to be very careful, you have to focus on cost, at underwriting cost. Your underwriting costs are the most important cost in this business. What can kill you in a credit business is your credit cost, it is not going to be your cost income ratio, and it is not going to be your cost of funds. If you are reasonably smart, it is okay. But if you can get your credit cost down and keep them under control then there is a huge opportunity.

Mono-line vs Multi-line:

Most NBFCs are fairly mono lines (either in housing finance or commercial vehicle or gold loan) and what we have found is if you look at the NBFC’s history in India, monolines grow very fast but also struggle across cycles because if you are a housing finance company and you think there is a lot of irrational stuff going on the financial industry and people are under pricing, will you be able to scale back the business? It is very hard to do because how do you give up growth? No credit company will be ok with the shrinking book. So you will continue to grow hoping that I will be smarter than the others, but you will not be able to escape the irrationality of the industry. However, if you are a broad base firm, which what the banks are, you can keep on reallocating your portfolio. Aditya Puri once remarked to me that when the auto finance industry got very irrational, there was a lot of undercutting going on and HDFC Bank scaled back, actually exited the auto finance business completely for 4 years and then they came back after that. Now if you are at HDFC Bank you have that option, but if you are only an auto finance company do you have that option? You have the sales force, you have all the relationships with the dealers and you can’t escape that. You can slow it down but you can’t escape that.

Lack of size is an advantage:

Finding a new niche is a lot harder for larger banks. For example, microfinance companies like Equitas or Ujjivan is happy to build a Rs. 4000–5000 crore book over 8 year and be happy over that. But it is hard for a bank to say that I am going to spend 8 years figuring out the micro finance market and build an 8–10,000 crore book though it can be very profitable. The scale is actually starting to work against them in new emerging opportunities. So while we are seeing these untapped segments in the credit market, each of them is at a size of where it is exciting for building a 3-4-5-7 or 8000 crore book. But you can’t build a Rs. 30 – 40,000 crore book in any one segment. Lack of size is an advantage because we can go after smaller and niche opportunities and you have seen a lot of other NBFCs and the credit firms have also gone after that. The only bank who has done this very well is the HDFC Bank. It is the only bank which will a see Rs. three thousand crore opportunity and go after it. So whether it is gold loan or a micro finance loan they are not leaving that behind. So amongst all the banks it is the only bank I have seen which can go after this sub scale opportunities and build expertise in that and that been the magic they have. Twenty years ago when the broker accounts was a small part, the first one to maintain and build that line was HDFC Bank and their ability has been to go after the smaller segments.

Lessons from 2008 retail loan crisis:

Even in 2008 when there was a retail banking crisis, 80% of that was in small ticket personal loan, what is called STPL, that time and everybody from GE Capital to Fullerton to ICICI to HSBC everybody had a large part of STPL book and there was craziness because the same guy was actually borrowing from 8 people. You didn’t have the credit bureau then and in fact people like Bajaj benefited out of that unsecured market collapse as everybody emptied out of that space except the HDFC Bank. So if I go back to 2011, the only players left in unsecured consumer loans were HDFC and Bajaj. Idea in credit is to pick up early warning signal like we ourselves have gone and analyzed the 2008 STPL market and there were 2 – 3 firms which really got stressed. But you know large part of stress happened when everybody else slowed down and scaled back, they continued for 3 more quarters and the 3 more quarters was what actually killed them. So the idea is to see the early stress and scale back which is what I keep on emphasising and lot of our risk focuses on analytics and we work with CIBIL and everybody else to see that stress.

Scaling back is very important in credit business:

One good thing about credit markets in India is that there have been pockets like STPL in 2008, Project finance now and project finance in 89–90–91, 2000–2001, 2002-2003 was also project finance. It was auto finance is 96–97–98. There are always pockets and that is what we worry about the most that can it happen in SME and at that time our idea is that a) it should not be a large part of our book and b) can you scale back? Actually even in structured credit in 2008 we had a Rs. 1,100 crore book. By end of 2008 it became Rs. 400 crore. We shrank back that book in that time because of the market volatility post Lehman. So the ability to manage your risk and shrink it back is equally important. I remember I was talking to Uday Kotak and he said in 1999–2000 when all NBFCs failed, Kotak survived and one of the reasons is that they scaled back their business.

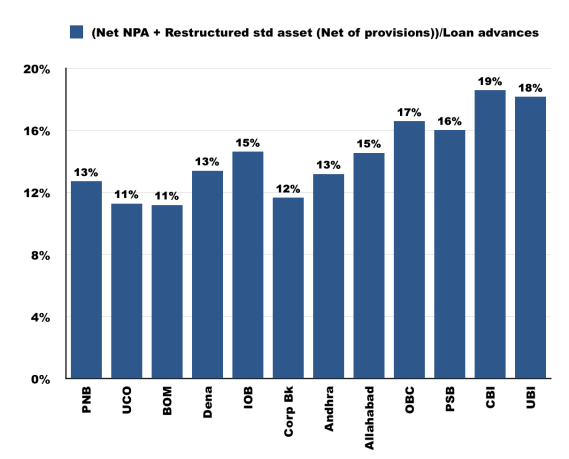

Wholesale credit book and NPAs:

If you analyze the NPA issue going on in the banks right now, which is mostly on the wholesale side, but 80% of the NPA issue is around project finance and frauds. So if you take the frauds like what is happening in REI Agro what happened in Deccan Chronicle and all of that, and if you take the project finance whether it is power, whether it is coal, whether it is mining, whether it is roads because approvals didn’t come, projects were over invoiced or whatever else were the reasons, 80% of the problem is project finance. Quite a few of our senior management started our career in project finance and even 25 years ago project finance was always risky. Project finance is never without risk in India and one of the reason all of us have avoided it is because at 13–14% interest rate you are not getting compensated enough for that; there is no risk reward in project finance but you can get scale in project finance easily, you can put Rs. 1,000 or 2,000 or 5,000 crore to work in the project finance opportunity quickly to gain scale. But if you avoid project finance, then wholesale credit books or corporate credit books even in IndusInd Bank, Kotak, Deutsche Bank etc. are not doing badly. So anybody who avoided project finance and frauds has been ok.

Real estate financing:

One of the other significant changes that has happened is, banks are becoming more conscious of risk based pricing. This entire NPA mess is forcing banks; banks are also saying I am not going to give money at 12-13%. So anywhere, normally these real estate guys would borrow from a non-bank at 100–200 basis points higher than they can get in the bank because bank has all these other issues. The banks are now starting to push this out of the banking part and your largest risk in real estate developer financing is execution risk. When you do a real-estate residential project, and we do only post approvals so usually there is no approval risk. If you take approval risk you can get a higher yield but if you do post approval, your only real risk is execution risk. It is not price risk at that level. You are 2x collateralized and unless there is a real estate collapse like an Asian crisis happens in India and suddenly the real-estate fall by 50–60 % which is not something that we think can happen in India given the way the economy is. In fact it has been improving. In the last one year even housing market has started to crawl back. Commercial real estate improved one year ago and this quarter housing also did really well and again, over the years I have seen one thing, the way night follows day, real-estate market follows stock market. So, if the stock market is going to be robust for the next couple of years, because real-estate market has not gone anywhere for 7–8 years, this is the biggest de-risking that has happened. Commercial yields are starting to inch-up but again idea is not to be too optimistic. Select your counter parties very carefully. If you get good counter parties and your collateral is good, you are ok. Some projects will be slower so your project execution risk may be there. The whole market of real- estate residential developers’ credit is about Rs. 100–120,000 crore market per year. HDFC is about Rs. 40–45,000 crore, Indiabulls is another Rs. 17-18,000 crore, Ajay Piramal’s group is about Rs. 14–15,000 crore and we are a Rs. 5,000 crore in that and that’s a fairly good market. Not a lot of people have lost money in that. The project have got stuck but on the credit side very few cases of default.

Profitability in urban home loan& LAP segment eroded:

We all NBFCs talk to each other and you know people who are handling products they are friends all over. Currently there is no stress building up. Their profitability has eroded from the home loan market. So home loan, especially urban salaried home loans, there is no profitability. We are not seeing increase in NPAs in that. In fact metros have becomes fairly competitive on both LAP and home loans but the tier 2 tier 3 cities we are not seeing stress getting to build up beyond what is the normal range and it is partly analytics and partly also the craziness that we saw even in the home loan market in 2008 with 100% LTV and all are anyway not allowed any more. We are not seeing that kind of behavior. In fact underwriting discipline has still been fairly good and partly aided by the fact that people are able to grow without making compromises. It is not like 2008–09 where you had to make compromises in terms of your underwriting standard to grow. It is not just our experience, when we talk to everybody and you all will also know that people are saying that we are not getting the push to scale back the standards. In fact if you saw our LTV, it has only come down. So we are not seeing it but it is a worry that should always be there and you should constantly look out for that.

Economic incentive for banks to sell NPA’s to ARC business:

ARC will continue to grow for the next couple of years because the banks usually sell the assets after the second year because the provision impact is the most after the second year because they provide 15% in first year, 30% in second year and goes upto 100% soon. The irony is that very often, the NPAs are not beyond recovery. If I gave to you home loan and it became NPA, it won’t become zero and eventually one should be able to recover 30, 40, 50 percent. For the bank it makes a lot of sense to sell to an ARC even at 40 cents to a dollar and avoid the last 40-50% NPA provision because once they sell it to ARC, then they don’t have to provide anymore.

[My Note: This explains the excitement around the ARC business with slew of partnerships between indian entities like SBI, ICICI, Kotak, Piramal and foreign capital providers. If you are interested in understanding the business model of ARC – better read pages 29-31 in the transcript].

III. About Edelweiss business lines:

Credit and non – credit approach:

There is something that we are trying to implement in a different way. We believe having a good mix of credit and non – credit is the way to build truly a very scalable kind of a model. Most of the NBFCs are very credit oriented and credit is obviously the big part of the opportunity. Obviously currently credit is very hot but over a long term we have seen India growing the way other economies have grown and having the non-credit side of equation also gives you a balance and gives you a lot more sustained profitability.

Game plan for building the retail book:

We see lot of opportunity in Retail mortgage, agri & rural financing, SME business. Most of the verticals were started about 3–4 years ago and we are still understanding. Our strategy has been to take 4-5 years to understand the segment and then you start scaling up. As I said, at our size we can afford these things. So our whole idea is thinking like a bank having about 5–6-7 sectors where we can keep on reallocating capital.

Going through the grind while building business:

We started hiring people for our retail finance business, in 2011–2012. We were very clear that retail would take 8–10 years to build. So I do think that even now retail business in Edelweiss is under stated in the profit because we are still in the investment phase. We started our retail credit business in 2011 and only this year we have hit 10–11% RoE. We think it is a 20-22% RoE opportunity. Scale matters a lot because we have studied all the retail finance service companies and your cost income ratio and your scale are inversely proportional. What we say in all retail businesses you have the front book and the back book and the acquisition cost of the front book is what impacts your current P&L and the back book is what really adds to P&L. All retail finance companies invest a lot in building the back book and it takes you 8–10 years to build the back book and you have to go through the grind. We started this in 2012 and from 2012 onwards it has been good growth and we are still continuing to invest in retail. We do feel confident that as the retail is getting scaled up, there is still a lot more opportunity in front of us.

Game plan for non-credit side:

On the non-credit side we still have a high cost to income ratio of 74% and on long term basis we think we should be 50–60% because as you get scale it improves. But currently we are investing in building scale so we are growing fairly fast. We want to grow this business at a Net Revenue level at 35– 40%. It still makes only 22% RoE, usually non-credit should be between 30– 40% RoE. We think it will be another couple of years away before we get that scale to start generating or eking out or harvesting the profitably out of this.

Game plan for Insurance business:

On a long-term basis, to build an insurance company, you need to have agency model. If you look at most large good insurance companies around the world over the last 40-50 years, you will find very few companies, which have been built around the banca model. But the problem with agency is that it is expensive and it is a drag on your profitability, capital and cash flow. However, on a long-term basis, the profitability of selling traditional products through agents is the highest. So in a way, you are buying a new more fuel-efficient car which is very expensive. So you are spending a large amount upfront, but you get the returns over the long term.

Balance sheet management:

We also focus a lot on liquidity cushion because as you know we are not a part of a large industrial house or a large business group. In that sense we operate like a standalone bank with a large part of assets in treasury. Our ALCO focuses a lot on liquidity management and in fact the liquidity guidelines that we internally follow are the Basel 3 guidelines. We have almost 9% of our assets in unencumbered cash assets available to us on an overnight basis. We are able to do this because we have a treasury approach to this which most of the NBFCs do not have, though they are starting to build now.

Warehousing and Agri commodity financing business:

The reason we are in agri services (Warehouse & collateral managment) is because we want to build agri credit business and we have realized that without an agri service as an arm you can’t build an agri credit business, as your risk will not be easy to manage. Agri financing is usually short-term, it is usually between 3 months to maximum 1 year, because a lot of this are self liquadating assets. So our whole strategy is we become warehouse managers & collateral managers, and after that we fund goods which are in our warehouses. We believe it is an very innovative robust model for financial intermediation in commodities.

Warehousing industry is getting organized and we have WDRA (Warehousing Development and Regulatory Authority). Eventually warehouses should be like NSDL– CDSL. If there are goods lying in the warehouse then you can be certain that the goods are there and they are clean and that is where India needs to go. The good news is that the warehousing industry especially for agri is starting to get organized. Lot of the PE money is starting to go into this segment, which is the first indicator that this is getting organized and all are high quality companies that are getting built. This is a 5–10 year trend.

Fairfax paid Rs. 1,100 crore for NCML with 1.3–1.4 million tons capacity and they make about Rs. 28–30 crore PAT and they paid almost 40X of that because they see opportunity there.

Fairfax paid Rs. 1,100 crore for NCML with 1.3–1.4 million tons capacity and they make about Rs. 28–30 crore PAT and they paid almost 40X of that because they see opportunity there.

All banks are keen to do this (agri credit). Our estimate currently is that this is a Rs. 100,000 crore credit opportunity for the organized market and currently banks do anything between Rs. 20–40,000 crore and this keeps on fluctuating because ultimately a warehouse receipt business is a risky business and in the past ICICI had issues, all banks have had issues, NSEL is another one, because we are still not at a stage where a warehouse receipt is something you know that the goods are behind it as we all have found out after NSEL. An organized warehouse manager is something that banks want and banks are appointing others and us as collateral managers. There is a feeling that the WDRA is going to impose capital adequacy norms on the warehouses managers, which will be good. It is in the proposal.

We are not into warehousing and logistic business. We started doing a little bit of agri credit, built our first Rs. 100 crore book then realized that there is a lot of risk management required when the goods are lying in the third party warehouse. Hence we stopped that and went back to drawing board, which took a lot of time to convince our board. On a long-term basis we don’t see ourselves as a warehouse manager; we just had to do it. Coincidently we may have ended up building a standalone good business but our long term idea was that if there is a warehousing logistics management opportunity we will go on that part and we will be sponsors of that but we wanted to use that base for building an agri-credit business as our attempt has always been to find credit opportunities where you are not competing head-on with banks because banks have a cost of capital advantage. The idea is to find things where you don’t compete with banks but you collaborate with them. A lot of the Agri credit we are doing we expect that about a third of that will be priority sector. So now a lot of banks come to us saying can you help us expand our agri portfolio? We don’t want to do farmer loans but here biggest thing is the collateral is in your control because if it is not in your control then risk multiplies manifold. Unlike a car which has its identification or a house which has an identification, a bag of wheat has no identification which is the biggest risk at the end of the day in this particular sector. If that risk is conquered, this is a Rs. 100000 crore market and think about it, for 4% spread on Rs. 100000 crore market is Rs. 4000 crore. Opportunity is out there and it is a fairly big one. All banks, a lot of global financial institutions want to come and partner with us.

Looking forward to your thoughts and comments 🙂. My twitter handle (@eeswardev).

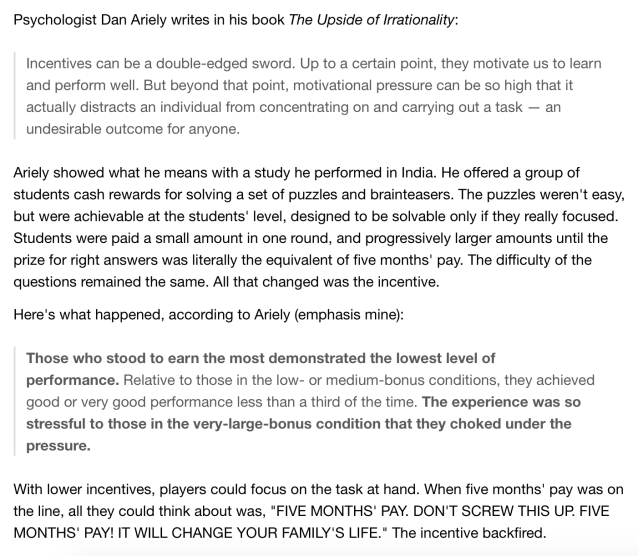

High-powered Incentives:

High-powered Incentives:

[Note: I filled-in best possible guess for the future auction in August and September 2016. In October, there will not be auction as last person standing will get to take 4.75 lakhs].

[Note: I filled-in best possible guess for the future auction in August and September 2016. In October, there will not be auction as last person standing will get to take 4.75 lakhs].

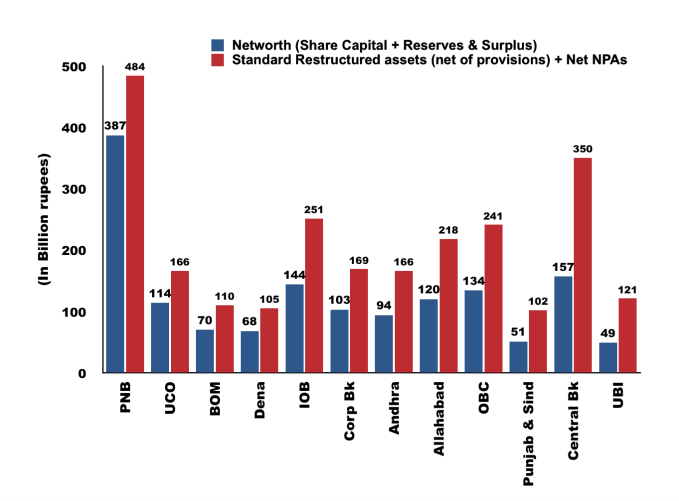

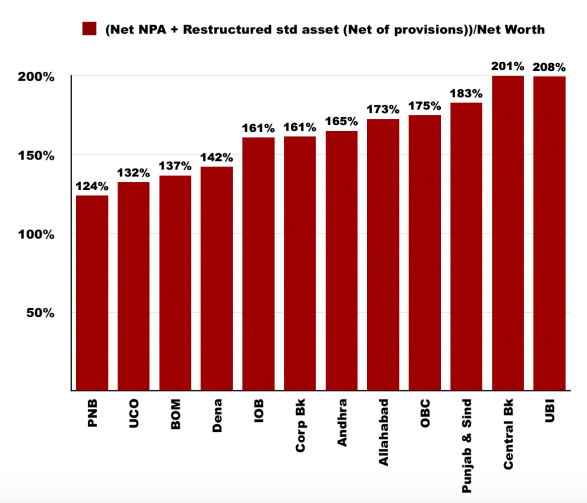

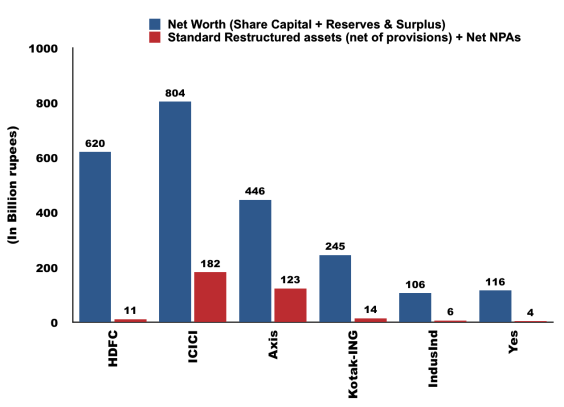

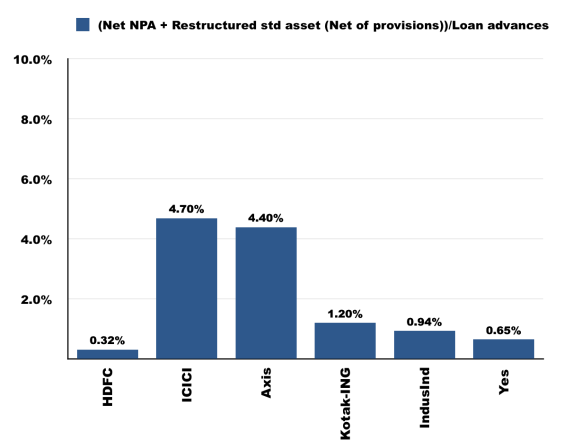

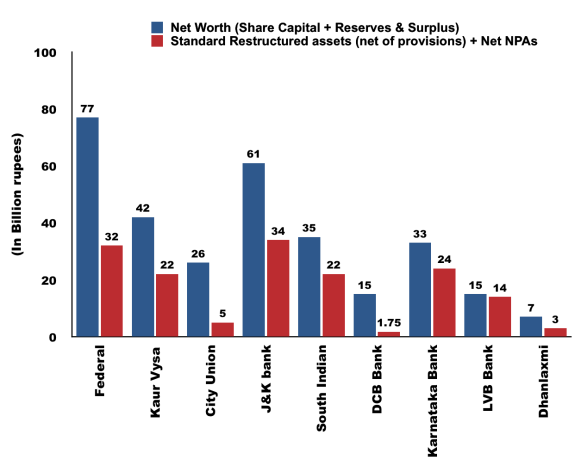

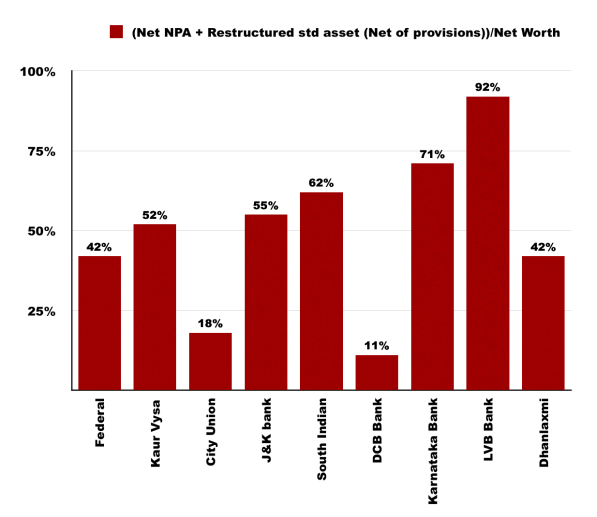

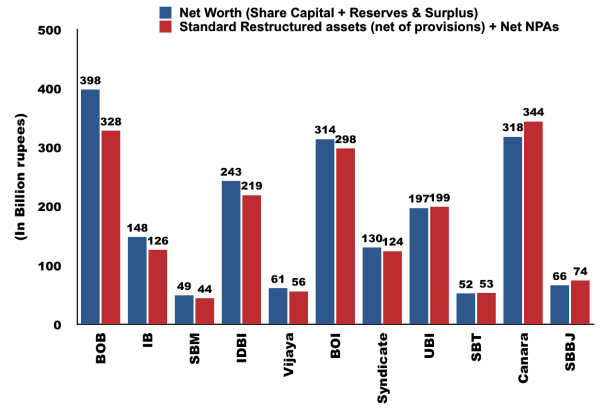

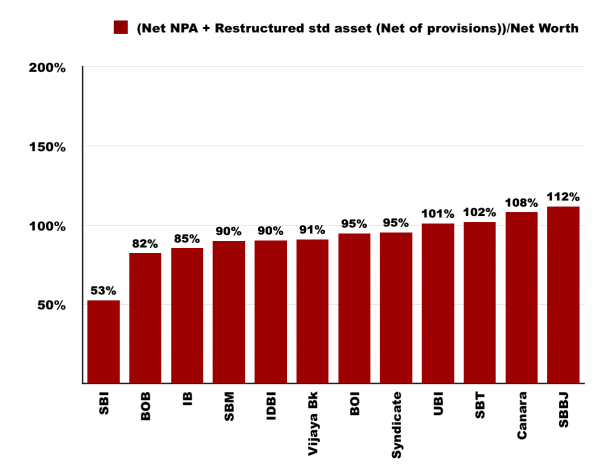

[Note: For example, in the case of Federal Bank, bad assets constitutes 42% of its entire Net Worth].

[Note: For example, in the case of Federal Bank, bad assets constitutes 42% of its entire Net Worth].

[Note: For example, in the case of SBI, bad assets constitutes 53% of its entire Net Worth].

[Note: For example, in the case of SBI, bad assets constitutes 53% of its entire Net Worth].