Special situation investing involves participating in variety of corporate actions like buyback, rights issue, demerger, etc. These are low-risk arbitrage opportunities which can act as kicker to investor’s core portfolio. In this blogpost, I am going to concentrate on demerger/spin-offs.

Demerger/Spin-offs happens for two broad reasons:

- Due to conglomerate nature or historical diversification steps, company could be operating in two completely different areas of businesses. Demerger/Spin-offs can help to get better valuation (no more holding company or conglomerate discount) and unlock parent company’s value. It also gives focused management bandwidth to each business to grow and scale up. Recent examples: Crompton greaves, Max India, and Transport corporation of India

- Sometimes, parent company might be struggling with debt, which holds back the core operating performance of the company. Hence, the management sandbag one of its divisions with debt and spin them off. This will liberate the other operating company from the debt and help them to achieve better valuation. Recent examples: Future enterprises became holding company with loads of debt and some investments in group companies whereas Future retail was spun-off with minimal debt. Same is the case with Sintex Industries where textile division had loads of debt and poor operating metrics when compared to Sintex plastics.

First category: It is a plain vanilla demerger but for some reason, Mr. Market mis-prices them even after the management’s demerger announcement. It usually takes 10-12 months from board approval to record date announcement. I believe Mr. Market underestimates what a focussed management bandwidth can do to the fortunes of the company. Market will offer an opportunity to enter these demerger stories at some point in time during this 10-12 months period.

Peter Lynch on Spin-offs:

“Spinoffs often result in astoundingly lucrative investments. Parent companies do not want to spin off divisions that will go on to fail as this would reflect poorly on the parent. Once these companies are granted their independence, the new management, free to run its own show, can cut costs and take creative measures that improve the near-term and long-term earnings. Spinoffs get little attention from Wall Street and they are usually misunderstood by investors. This all bodes well for future returns. Spinoffs are a fertile area for amateur shareholders. Lynch recommends looking for spin-offs with insider buying as it will confirm management believes in the spin-off’s long term potential”.

Second category: Sometimes, Mr. Market favor one business division much more than the other one. It could be due to high debt, small market capitalization, lack of complete information regarding the assets it holds. This will result in forced selling by the market participant. For example, a large mutual fund/FII’s mandate doesn’t allow them to hold companies more than 500 crores market cap. The discarded business division could be worth lot more than the current depressed price offered by market.

Howard Marks on Forced Selling:

“The absolute best buying opportunities come when asset holders are forced to sell, and in those crises they were present in large numbers. Believe me, there is nothing better than buying from someone who has to sell regardless of price. From time to time, holders become forced sellers for reasons like these:

- The funds they manage experience withdrawals

- Their portfolio holdings violate investment guidelines

- They receive margin calls because the value of their assets fails to satisfy requirements agreed to in contracts with their lenders”

Joel Greenblatt on Spin-off:

“Believe it or not, far from being a one-time insight, tremendous leverage is an attribute found in many spinoff situations. Remember, one of the primary reasons a corporation may choose to spin off a particular business is its desire to receive value for a business it deems undesirable and troublesome to sell. What better way to extract value from a spin-off than to palm off some of the parent company’s debt onto the spin-off’s balance sheet? Every dollar of debt transferred to the new spinoff company adds a dollar of value to the parent.

The result of this process is the creation of a large number of inordinately leverage spinoffs. Though the market may value the equity in one of these spinoffs at $1 per every $5, $6 or even $10 of corporate debt in the newly created spin-off, $1 is also the amount of your maximum loss. Individual investors are not responsible for the debts of a corporation. Say what you will about the risks of investing in such companies, the rewards of sound reasoning and good research are vastly multiplied when applied in these leveraged circumstances. Tremendous leverage would magnify our returns if spinoff turned out, for some reason, to be more attractive than its initial appearances indicated”

Seth Klarman on Spin-off:

“The behavior of institutional investors, dictated by constraints on their behavior, can sometimes cause stock prices to depart from underlying value. Institutional selling of a low-priced small-capitalization spinoff is one such example. Many parent-company shareholders receiving shares in a spinoff choose to sell quickly, often for the same reasons that the parent company divested itself of the subsidiary in the first place. Shareholders receiving the spin-off shares will find still other reasons to sell: they may know little or nothing about the business that was spun off and find it easier to sell than to learn; large institutional investors may deem the newly created entity too small to bother with; and index funds will sell regardless of price if the spinoff is not a member of their assigned index. There is typically a two to three month lag period during which the spin-off company’s financials have not been entered into financial databases and there will be very few analysts covering it. Thus, the stock could be the cheapest stock in the world during this time”

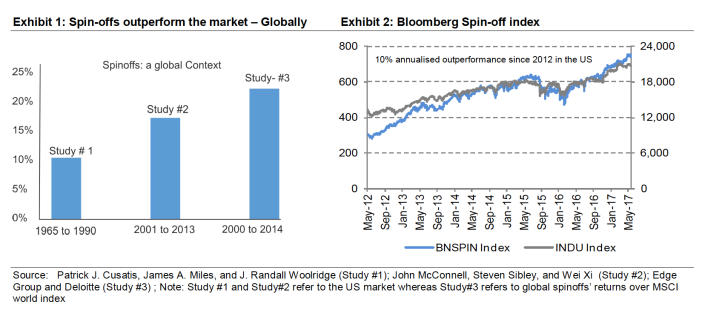

Historical data both in India and around the world points to better performance of spin-offs when compared to broader markets.

Empirical data on Spin-offs globally:

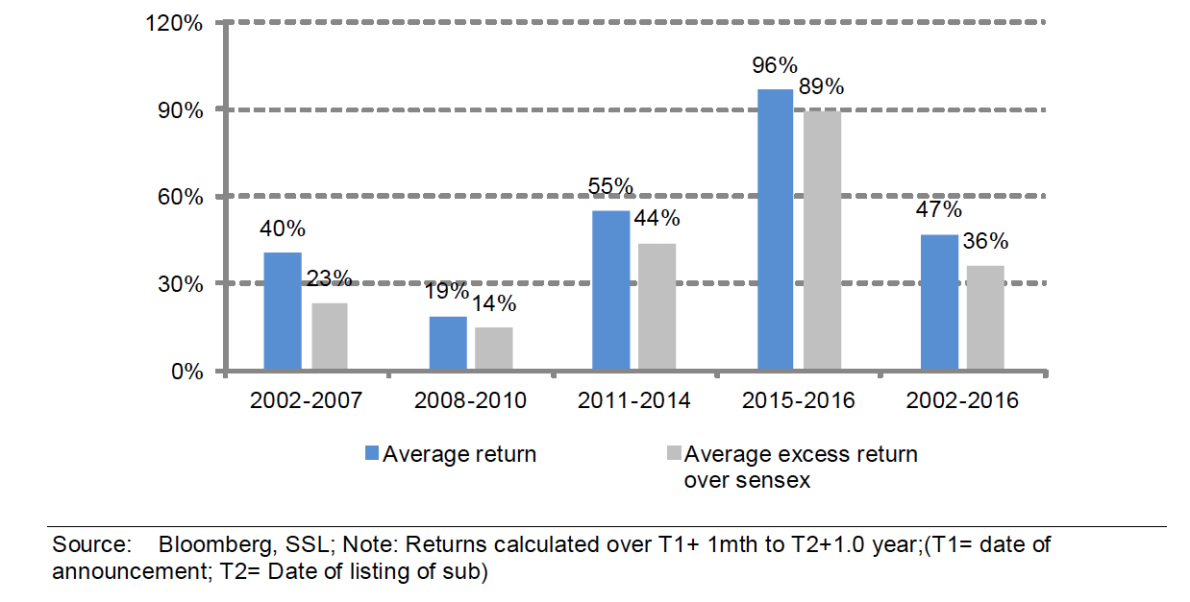

Empirical data on Spin-offs across market cycles in India:

My experience:

I have very limited experience in the demergers space. I started to focus on this segment for the past 3 years with reasonable success. Following are some of my experience:

- Crompton Greaves: Demerger of Consumer electrical division from parent CG power. Crompton was a very powerful brand in consumer electricals but management couldn’t focus, invest and grow the brand due to the distraction of poor operating performance of CG power overseas division. Management announced demerger and at the same time sold their stake to PE funds (Advent International and Temasek holdings). I believed new management can realize better value than the current management. Meanwhile, they appointed Shantanu Khosla as new MD who is veteran in P&G India signalling change in management focus. Hence i bought them between Jan and Feb 2016, with a simple assumption that new management focus can help to create better value for the Crompton brand. Investment worked out lot better than i initially thought.

- Transport Corporation of India: Demerger of TCI express division which caters to e-commerce verticals. Here both the parent and the demerged entity were equally good. Most Indian promoters has many children. In order to avoid conflict and give them better autonomy, promoters will demerge business division so that each children can steer an individual company better and scale them up. TCI and TCI express is a straightforward demerger. I bought 2-3 months before the record date for demerger and both equally performed well over the past one year.

- Future Enterprises: This was not my original idea. One of my friend shared his short thesis on the company: “Future enterprises is Complex spin off. Top 3 shareholders are ‘Consumer funds’ who are now forcefully selling the ‘Rental & Investment spinoff’ as it’s not in their mandate to hold non consumer stocks. Value of Investments (in Future lifestyle, Future Consumer, Logistics division, Insurance division) exceeds total debt. Management has promised to monetise assets and pare debt quickly which is key. Process has already begun. While the rental business is available free. Expecting huge cash flow from this business in coming quarters. I think the stock is worth more than CMP. Pure holding companies trade at discount but here management is planning to monetize the assets and pay off the debt. Hence value will migrate from debt side to equity side”.

- After reading his note, I looked at the shareholding pattern of the company. The amount of forced selling by FPI consumer funds was staggering. They wanted to get rid of their positions in the holding company before December year-end closing for investor’s reporting. Check out the following table:

|

Name of FPI |

Mar’16 | June’16 | Sep’16 | Dec’16 |

|

Arisaig India Fund |

8.14% |

7.32% | 6.41% |

<1% |

| WGI EM Fund | 2.77% | 2.49% | 1.12% |

<1% |

Based on the above info and company’s presentation’s, I bought Future Enterprises in Dec’16 and the investment turned out very good.

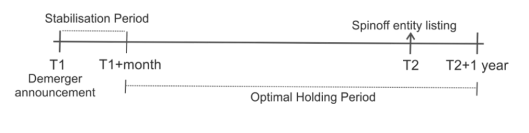

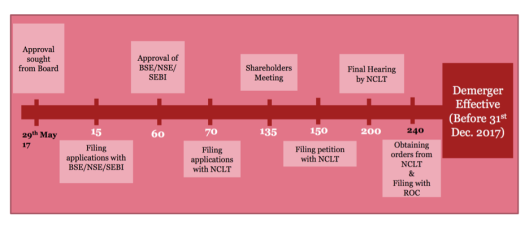

Timeline of demerger process in India:

[From a company’s presentation: Timeline is little optimistic (usually it takes 10-12 months instead of 8 months mentioned above). Just added to give an idea on steps involved in the process].

Demerger opportunities currently open:

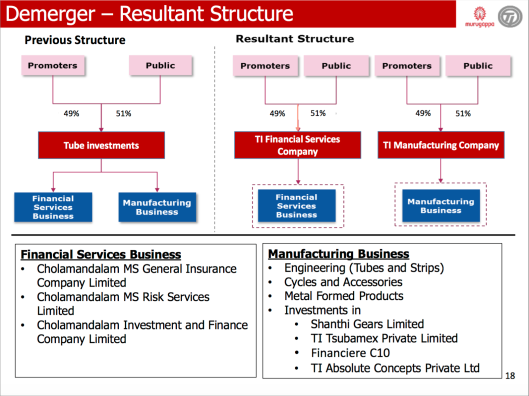

My thoughts on Tube Investments of India demerger:

As we can see from the above table, Tube Investments of India board announced demerger of manufacturing vertical from financial services on Nov 3, 2016 and currently it is close to getting NCLT approval. Record date would be around Sept 2017 and further listing of the demerged entity would be around Nov 2017. It is part of Murugappa’s group. Management is known for competence and integrity.

Recent company’s presentation is very informative. Have a look.

I did valuation analysis on July 1, 2017. Market cap = 12,500 crores.

Financial vertical = approximately 10,000 – 11,000 crores.

- Holds 46% stake in Chola finance. At CMP, it comes to 8000 crores. Let’s apply a holding company discount of 25% = comes to 6000 crores.

- TII holds 60% stake in Chola MS general insurance business. It is one of the better managed and consistently profit making general insurance business in India. Got captive customers in Chola finance for selling general insurance policies. In addition, in recent times, government opened up agri insurance business which gives more business opportunity for general insurance companies.

- None of the general insurance companies are listed. Hence we have to rely on secondary market valuation. In March 2016, TII sold 15% stake to Japanese JV partner Mitsui at a valuation of around 6500 crores. TII’s 60% stake comes to 3800-4000 crores. Demerger will happen sometime around August, 2017. Hence 18 month forward, one can assign 5000 crores. FY’17 TII’s 60% share of profits = 125 crores (growth of 60% over FY’16). For FY’18, i expect this division to post 155-160 crores (25% growth). 5000 crores valuation assigns around 30-32 PE which is reasonable considering general insurance business potential and scores of planned IPO listing in this space in FY’18.

Manufacturing vertical = approximately 4000 crores:

FY’16 Revenues = 4000 crores; EBIT = 260 crores (margin 6.3%). FY’17 revenues of 4200 crores & EBIT of 310 crores (7.3%). Most of the capex is done. FY’17 volumes of cycle division suffered little bit. Economic revival & better capacity utilization can push up the EBIT margins to 9-10%. Even if we value at 1X revenues/12X EBIT, its valuation approximately comes to 4000 crores. Got a debt of 650 crores – which is manageable given the cash flows.

Above calculation shows that roughly there is 25% valuation gap. I can see 2 trades here. First opportunity: Buy close to the NCLT verdict and hold for 12-18 months for decent returns. Another opportunity could be: After listing, market for some reason could favour finance division much more than manufacturing division and that can result in temporary mispricing which can be good entry point for decent returns.

Recent development: Murugappa group has a policy of rotation of CEO among various business divisions so that they don’t get attached to the business and mistreat it as their fiefdom rather than being a team player in the overall group activity. Group appointed Vellayan Subbiah as MD for Tube investments of India. He successfully turned around the Chola finance business over the past 5-6 years from their slumps. I believe this can booster dose for the better profitability of manufacturing vertical of Tube investments (Just a guess). Have a look at his profile.

Conclusion:

There is no single scientific reason/valuation metric behind better returns in demerger/spin-offs. It could be due to multitude of factors like better market perception, better management focus, better valuation due to forced selling etc. One additional indicator I track is insider’s behaviour. Sometimes, promoter will buy from open market or allot warrants indicating their intention to raise stake in these companies. I know that in the current red-hot market where small caps are flying thick & fast, average returns of 20-25% wont appeal to lot of people. But i still believe that investing around the special situations like demerger carries minimal risk and it is a useful tool to have in the portfolio.

However, everything is not rosy in the world of demerger. In recent times, IDFC bank demerger is one example where some of my friends made zero returns. Sometimes, management cancels the whole demerger process (Eg: Jasch Industries). Hence, it is important to pick and choose the company we want to associate with.

Resources:

- You can be a stock market genius – Joel Greenblatt [Chapter 2: Page # 53-128]

- Margin of Safety – Seth Klarman [Chapter 10: Page # 187-191]

- One up on wall street – Peter Lynch [Chapter 8: 133-136].

- SBI Capital Securities on demergers in India – Link

- Axis Capital research report on Tube investments of India – Link

Disclaimer: Please note that this is my investment journal. The main aim is to expose my investment thoughts to the scrutiny of fellow investors and improve the process thereby. It shall not be construed as an advise to buy/sell the stock.

Good article, good advice.

Only thing is that the stock has already appreciated around 40% and whether there is enough return available now is to be seen.

Wish this article would have appeared six months back.

LikeLike

My friend, articles are for self learning, not buy/Sell recommendation. Just learning opportunity to apply for future demergers

LikeLiked by 1 person

Thanks 🙂 Demerger was announced on Nov 3rd 2016 and it barely appreciated 15% since. I still believe there is some juice left if one held for 12-18 months but wont be big multibagger for sure.

LikeLike

Good article. Financial division will be priced more.

LikeLike

Thanks 🙂 That is the general perception – Lets see what Mr. Market does.

LikeLike

Add ANAnt Raj to that list

LikeLike

Missed it completely. Thanks for adding.

LikeLike

very good thought process, some portfolio managers have have a special PMS for special situation/ event,history tells many big investors have made good money in these type of investments.

Value unlocking is for sure going to happen but at what price we enter matters a lot .

if one can close their eyes on management (!) , then, out of the opportunities you have mentioned Reliance Capital seems to be okay.

But hoping, market gives us another chance to enter TI before November

LikeLike

Thanks for the kind words 🙂 Yes, at CMP, upside is not manifold – Can only give decent returns.

Agree on Reliance capital – conservative estimate shows that there is wide gap between intrinsic value and CMP. Beyond management, I could not get a good handle on the composition and quality of their loan books in home finance & commercial finance division. However, it will be a interesting demerger story to follow.

LikeLike

Excellant bossu, I really had fun reading it, it was backed up by good data and deep research. I am very happy and appreciate it very much

LikeLike

Thanks for the kind words 🙂 Happy Learning.

LikeLike

Hi,

Pl look into face value reduction and refer June 2017 results. If possible, pl share possible price discovery range.

Whether forced selling of fii who holds 12% due to demerger.

LikeLike