Tags

Traditionally, i avoided financial institutions due to the inherent leverage in its business model. Considering its immense potential for wealth creation, recently i started taking baby steps towards analyzing indian banking sector, its growth drivers, and future potential. In this two-part series, i will document some of the interesting things i learned (Don’t worry, i am not going to bore you with all the financial jargons in analyzing financial stocks 🙂 Rather i would like to pen down some of the ‘aha’ moments during the learning process).

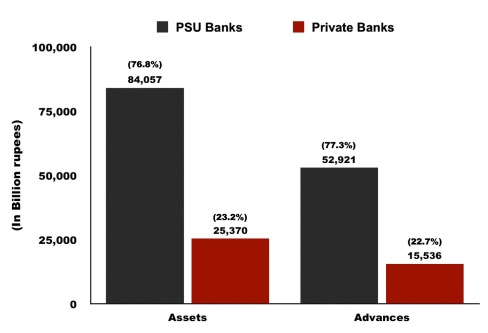

Indian Banking structure:

There are 27 public sector (PSU) banks and 20 private sector banks in India. However, majority of the assets and loan advances are controlled by PSU banks.

[Source: FY 2015 Bank Annual reports. Data excludes unlisted banks such as State bank of Hyderabad & State Bank of Patiala (PSUs) and Catholic Syrian bank & RBL (Private banks)]

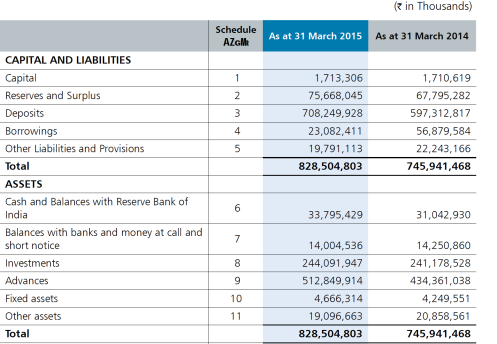

Balance sheet:

Understanding bank’s balance sheet is very crucial. Following is the snapshot of Federal bank’s balance sheet.

Liabilities side is dominated by bank’s Net Worth (Share capital + Reserves & Surplus), bank deposits, and market borrowings.

Assets side is dominated by Investments (Treasury operations) and Advances a.k.a loan advances (both corporate and retail loans). Loan advances are further classified into standard assets and non-performing assets (NPA). NPAs are loan accounts that are not paid for 90 days.

Generally bank’s Net Worth is levered (varies with each bank – approximately 8-12 times) with borrowings (bank deposits & market borrowings) to provide loan advances. In the above example, loan advances of Federal Bank is around 6.6 times its Net Worth. In other words, its entire Net Worth will be wiped out if 15% (1/6.6) of its loan advances turn bad assets and becomes not recoverable. Banks are generally valued at multiples of its book value (i.e. Net worth) depending on the bank’s return ratios and management’s capabilities. Before attaching multiples to Net Worth, we need to ascertain ‘true’ Net Worth by quantifying standard assets and bad assets.

PSU Banks:

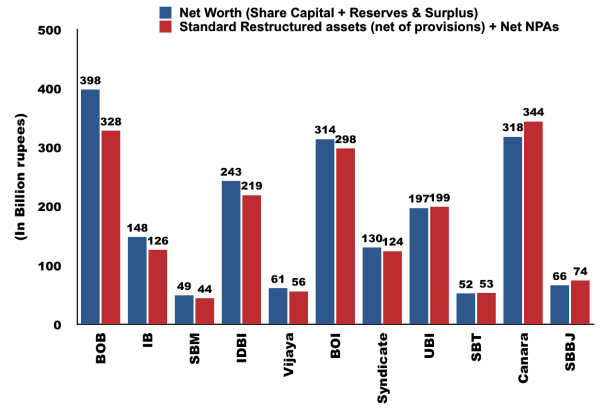

Instead of shortlisting good-performing banks, i inverted the process. First, i wanted to eliminate poorly-managed banks that contains lot of bad assets. Because more the bad assets, lesser will the ‘true’ Net Worth. I considered Net NPA’s and restructured standard assets net of provision as bad assets. I collated each bank’s Net Worth, Gross NPA’s, provisions for NPA’s, Net NPA’s, restructured standard assets (according to me, they are nothing but glorified NPA’s that are ever-greened due to lax attitude of regulator & bankers), provisions for restructured standard assets from its FY 2015 annual report. Lets look at numbers of 24 PSU banks loan advances in two separate sets.

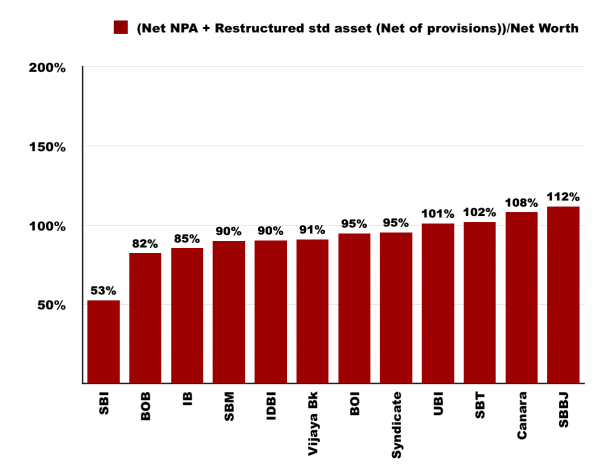

First set of PSU banks:

[Note: I removed SBI from above the chart as its assets are huge and skews the graph. Hard data: Standalone SBI’s Net Worth – 1284 bn and bad assets – 676 bn (Net NPA – 276 bn + Restructured std asset net of provision – 400 bn). But incidentally it has one of the better-managed loan book among PSUs as seen in the charts below. Its bad assets forms 5% of the loan advances only and its Net Worth is approximately twice that of bad assets].

[Note: For example, in the case of SBI, bad assets constitutes 53% of its entire Net Worth].

[Note: For example, in the case of SBI, bad assets constitutes 53% of its entire Net Worth].

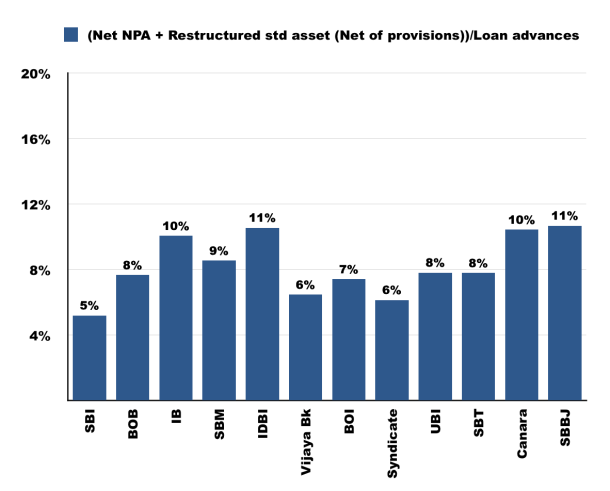

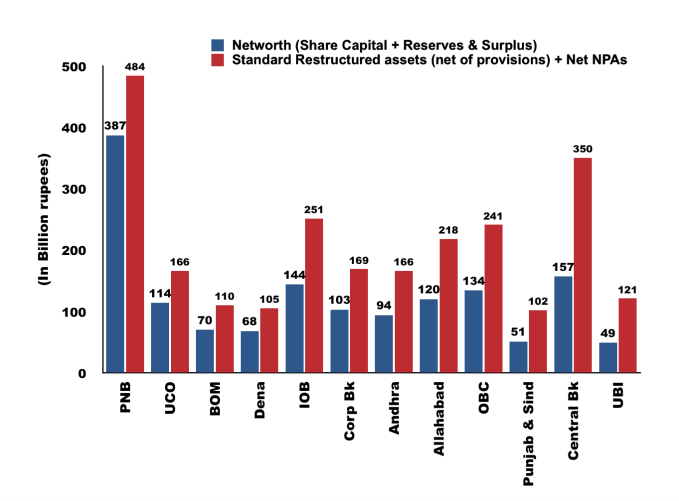

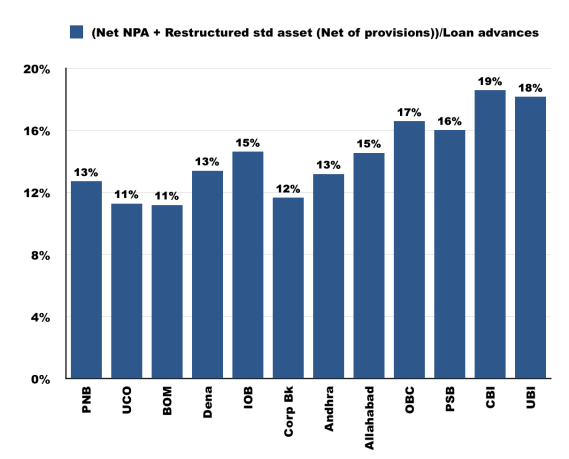

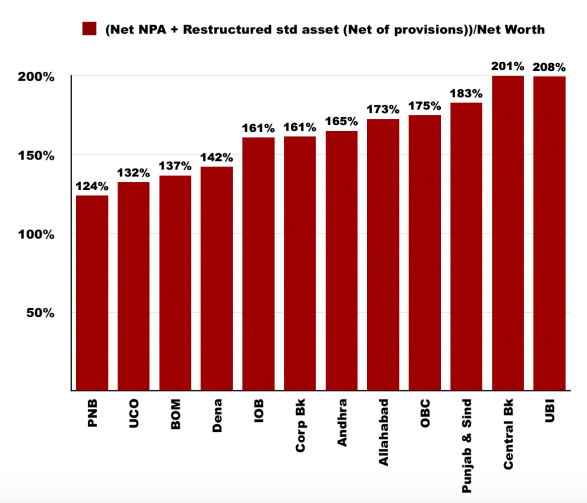

Second set of PSU banks:

[Note 1: For example, UBI’s bad assets is 2x its Net Worth. If it takes a 50% hair cut out of its bad assets (highly unlikely), its entire Net Worth will be wiped off].

[Note 2: In my twitter page, i shared my preliminary analysis. Here i inverted the ratio to provide better picture. Also, Numbers here are slightly different due to inadvertant minor error. Restructured loan book contains assets from both standard asset and NPA accounts (Thanks to @deepakshenoy for pointing out). I corrected it and included only restructured assets of standard loan book & Net NPA’s for the calculation of bad assets. I also netted of any provisions against those restructured standard assets. Still the numbers are scary 😮 and doesn’t change broader picture much].

As you can see from the above pictures, loan book of SBI and its associates are relatively (Only relatively !!!) better than other PSU banks. Some of the smaller PSU’s like Allahabad bank, Oriental bank of commerce, Punjab & Sind bank, Central bank of India, and Union of India are in dire straits with bad assets/loan advances >15% and its bad assets constitutes 1.75-2x Net Worth.

Equity dilution:

Equity dilution is principal enemy for the long-term investors in banks. PSU bank stocks are beaten down so much. There could be short-term 30-50% jump depending on developments such as marginal improvement in stressed sectors, extension of leniency by RBI or government package etc. But i am more interested in the long-term wealth creation and being novice in the market, i don’t have the ability to predict on the possible short-term movement. For me, putting finger on the bank’s ‘true’ Net Worth is crucial.

Lets be clear on one thing: None of the bank’s Net Worth is going to ZERO. Either government will re-capitalize or it will merge with relatively better PSU banks. Principal question: What will the hair-cut to the bank’s Net Worth due to the bad assets? According to CRISIL ratings, historically, about 35-40% of the restructured accounts have eventually defaulted. Lets be charitable and factor in 25% haircut.

In addition, bank needs additional capital of 25% to meet Basel-III recommendation and also to meet additional provisioning requirement due to RBI’s change in rules. In total, there is a real probability of approximately 40-50% equity dilution for long term investors.

Based on the above analysis, i eliminated all the PSU banks except SBI. I would re-examine them when all the things like recapitalization settle down. In recent times, i became very skeptical of turn-around stories. Being contrarian is very different from being contrarian & right. Success stories of turn-around stories are filled with survivorship bias. Generally investors who became contrarian early in a turn-around story are not alive to tell their story. My thumb rule for turn-around stories: Have a starter position – Let the management execution & business profitability determine your position size and not your wishful thinking. I would like to stick to this rule even if it means leaving some profits on the table.

In the part-2, i will document some of the interesting things i learned about the private sector banks and technological innovation in banking industry.

I attached data excel sheet. Feel free to download and play with the numbers. Let me know if you come across any mistakes or interesting observations [Note: All the numbers are collected from individual bank’s FY 2015 annual report. I generally don’t attach much to quarterly reports and analyst presentation – lot of things are swept under the mat. 2 Quarters were passed – some of the banks might have raised equity capital, sold bad assets to ARC, or recognized more bad assets – Please keep that caveat in mind].

Looking forward to your thoughts. Cheers 🙂

Pingback: Indian Banks – Part II | Ant Investor

Hi,

Excellent analysis and clear view of what is going to come. Would be interested in understanding how banks are going to sell off the npas as valuation is still an issue. Also how banks will improve by adopting technology. And finally how much of stressed assets can be sold to ARCs. The way ARCs are valuing assets will it not be challenged some time from now by borrowers?

LikeLike

Thanks for the comment 🙂

1. It is going to be up-hill task. Most of the NPAs are from Power and Steel sector. Both are plagued by multiple well-documented issues. Power – lack of fuel linkage and its customer i.e. State electricity board is in very bad shape. Even with UDAY scheme it will take 3 years to limp back to normalcy if everything works out as planned. Current buzz is around renewables – hence don’t know who will buy the coal & gas based power projects that are stranded. Steel sector is plagued by over-capacity and the current prices are killing the sector. Most likely will be just follow standard ‘pretend and extend’ by kicking the can down the road and allow these zombies to fester PSU banks for years to come.

2. Lot of exciting stuff happening around fintech and any one with capital can purchase them. But mindset to adopt to the technological change is very difficult. Management must have vision on trends and HR bandwidth to train & equip employees. Unfortunately situation is very bleak on this front for PSU banks. It is not just the CEO that matters – entire top management have vital role to play.

3. In India, there are very few ARC’s (I heard only ARCIL and Edelweiss in the news) and they are woefully short of capital to handle this deluge of NPA’s. Deeper pockets and greater expertise in managing asset is needed. At present, not much can be sold to ARCs.

LikeLike

Turnarounds seldom turn, as a wise man said.

Great post.

LikeLike

Hi,

Great article, One quick question, How did you calculate leverage of Federal Bank as 6.6 times. As per my understanding (and apologies if my formula is incorrect)

Share Capital + Reserves & Surpls – INR 76 Billion

Deposit & Market Borrowings – INR 731 Billion

Leverage is closer to 10X, could you please educate me if my understanding is correct.

Many Thanks

Nikhil

LikeLike

You are right. Bank was leveraged by 10x. But due to regulations it can lend only 60-65% of it and balance is maintained in treasury operations as mandated by RBI. Hence I thought it would be more appropriate to compare Net worth (77.3 bn) with loan advances (512 bn) to get true picture of leverage. I corrected original text for better clarity – please let me know whether it makes sense now. Thanks for pointing out.

LikeLike

Hi,

Thanks for reverting. Agree to your point that leverage should be calculated on Advances and not on Deposit & Borrowings given that Banks have to maintain CRR/SLR, thus providing some cushion on their lending practices. However, couple of follow up questions: What activities does treasury operations constitute and how do bank raise funds for treasury, given that treasury generally yield between 7-8% roughly, while loans yields are higher, wouldn’t it be more prudent for banks to disburse loans rather than deploy funds for treasury.

Apologies if the questions are too basic or generic, however some color from your end will be helpful. Thank You

LikeLike

Hi Nikhil, We all are in various stages of learning. In fact, questions help me to have better clarity on the subject.

Presented below simplified version of bank balance sheet (i.e. the way I understand – not an expert in this field) – refer to Federal bank balance sheet for clarity

Liability side (Rs. 100):

1. Equity Capital & Reserves – 10/-

2. Bank deposits and market borrowings – 90/-

Asset side (i.e. how it deploys Rs. 100):

1. Cash & Balances with RBI – Rs. 4/- – This is basically Cash Reserve Ratio (CRR) – Regulatory requirement – cash deposited with RBI and yields nothing.

2. Investments – around Rs. 30/- This is the treasury operation we are talking about – its main function is to manage bank’s liquidity at all times – Out of 30/-, 21.5/- is Statutory Liquidity Ratio (SLR), regulatory requirement where RBI mandates banks to invest in G-Sec. Remaining amount can be invested in bonds & financial instruments with different maturities and bank can book profit out of the trading activity time-to-time. This is to mainly help the bank to overcome emergency situation when lot of bank lenders (i.e. depositors) ask money at once – It simply can’t say that I lent all the money. At that time, bank should be able to liquidate the bond portfolio in short notice and give back the money they deposited. Most of the time, bank matches the deposit tenure (lets say 3 year fixed deposit) with the lending tenure (lets say 24-30 months of 2-wheeler loan). But sometimes, asset-liability mismatch happens. Hence here higher returns is not important, liquidity is utmost important. This ‘investments’ amount varies time-to-time depending RBI SLR requirement and economic situation. If economy and liquidity is great: Treasury branch will keep less money (like Rs. 5 to 6/- + RBI’s SLR requirement) and let the lending branch to lend more.

3. Advances – around Rs. 62/- this is where retail and corporate lending takes place. Percentage varies from 60 to 65/- depending on the economic situation. If the bank feels there are more opportunities, it may increase the percentage.

4. Fixed and other assets – around Rs.4/- – Bank building, furniture’s and technology assets deployed etc.

Let me know if it clears your doubt.

LikeLike

Thanks. This example is really helpful.

Please do keep blogging more and share your learning with others. Many Thanks Nikhil

LikeLike

Good job. I liked the analysis

LikeLike

Thanks 🙂 Happy to hear.

LikeLike

Pingback: Indian Banks – Part I | rberyblog

Great analysis…. keep up the good work!

LikeLike

Thanks for the kind words 🙂

LikeLike

Good analysis. As per your analysis, SBBJ much worse than Syndicate Bank…both declared results…one going up, other down. That’s how market reacts…short-term operators and manipulation. IMO, Syndicate Bank is a multiplier…max 1-2 quarters.

LikeLike

Pingback: Indian Financial Landscape through the eyes of Rashesh Shah (Edelweiss) | Ant Investor

Nice article. cleared many basic concepts about banking. thank u soo much.

LikeLike

Good work as always! Simplest way to explain banking. If possible, please extend the scope to explain Tier-1,Tier-II capital using same Federal Bank’s Balance Sheet example.

LikeLike