Tags

In Part-I, I shared my preliminary analysis of PSU banks loan book. Even if the PSU banks overcome the bad assets and recapitalization woes, its future growth potential appears less than optimistic due to the recent advances in the technological innovation around banking industry.

Broadly there are 3 vital pillars in managing financial services and each of them undergoing profound changes:

- Facilitating Transactions – Fintech companies will make this vertical more and more commoditized. Most manpower in PSU banks are dedicated to this vertical whose relevance will wane in future.

- Pricing ‘risk’ – Fintech companies are trying to break open this vertical with models, artificial intelligence, data analytics etc. However, we all know what happened last time when financial world used models to price the risk [Hello 2008 :-)]. They have to undergo atleast one financial cycle to prove its worth. Local knowledge and real world judgement on pricing the risk will still be crucial.

- Workforce skill-set – Managing human resource, providing training in evolving technologies to improve customer service and to manage risk are very important. This is an area where large private sector banks has an definitive edge over PSU banks and even some of the smaller old-age private sector banks.

Private sector banks:

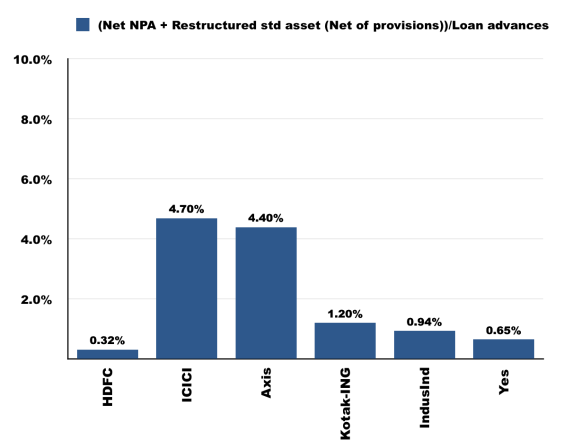

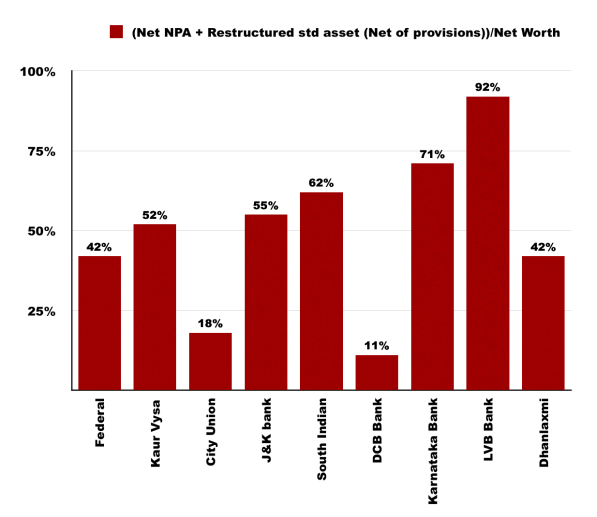

Lets first look at the loan books of private sector banks and weed out poorly-managed banks to arrive at the shortlist for further analysis. As i said in part-I, I considered Net NPA’s and restructured standard assets net of provision as bad assets.

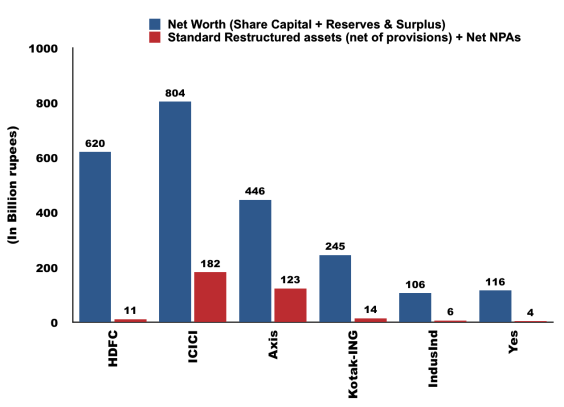

Larger Private banks:

We can clearly see why HDFC bank always trades at premium. It has got ultra-clean loan book with paltry bad assets. Bad assets of ICICI and Axis bank constitutes approximately 25% of its Net Worth. Quality difference in the loan book between HDFC bank and ICICI & Axis is clearly visible.

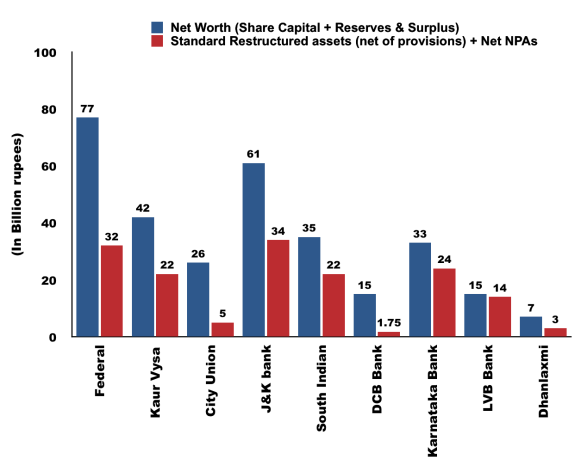

Smaller private banks:

[Note: For example, in the case of Federal Bank, bad assets constitutes 42% of its entire Net Worth].

[Note: For example, in the case of Federal Bank, bad assets constitutes 42% of its entire Net Worth].

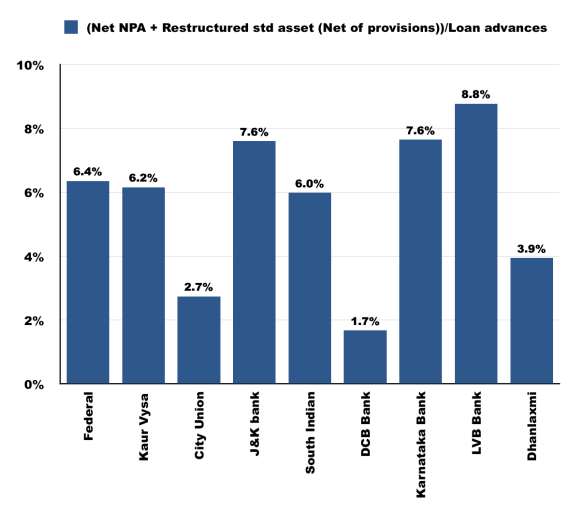

Debacle of Dhanlaxmi bank is well-known and hence lets exclude it. Except, City Union bank and DCB bank most of them are afflicted with bad loans problem. Barring these exceptions, bad assets constitutes 6-8% of the bank’s loan advances. It will hobble them for a while and higher than usual equity dilution can’t be ruled out.

Key points from long-term investing perspective:

- Better not to look at the PSU banks further, except SBI. In addition, probably SBI is the only PSU bank that has strong presence in asset management, insurance and investment banking vertical. Added it to watchlist.

- Among larger private sector banks, HDFC, Kotak, IndusInd, Yes bank needs to be delved deeply.

- Although Axis and ICICI bank are hobbled by bad assets, they have excellent retail banking franchise. Added both of them to watchlist – will closely monitor developments on asset quality front.

- Given the huge potential of financial sector in India, couple of smaller private banks may break out from the pack. DCB and City union bank needs to be analyzed further.

I attached private sector bank’s data excel sheet. Feel free to download and play with the numbers. Let me know if you come across any mistakes or interesting observations [Note: All the numbers are collected from individual bank’s FY 2015 annual report. I used only standalone numbers for comparable purpose. For Kotak-ING combined, i took FY’15 Kotak bank standalone + FY’15 Kotak Mahindra Prime subsidiary (which does car financing) + FY’14 ING Vysa (FY’15 annual report is not available due to merger)].

Looking forward to your thoughts. Cheers 🙂

Pingback: Indian Banks – Part I | Ant Investor

Any thoughts on new banks like IDFC

LikeLike

Have to wait for first annual report. Management made huge provision for infra assets when transitioning from NBFC to bank. One real plus: Looks CEO Rajiv Lall is of top-notch. He has clearly laid out strategy for the bank that makes lot of sense. Lets wait for the signs of management execution and also more info on troubled assets.

LikeLiked by 1 person

Very Well analyzed. As Warren Buffet cautions in his !990 letter to shareholders States-

“The banking business is no favorite of ours. When assets are

twenty times equity – a common ratio in this industry – mistakes

that involve only a small portion of assets can destroy a major

portion of equity. And mistakes have been the rule rather than

the exception at many major banks. Most have resulted from a

managerial failing that we described last year when discussing

the “institutional imperative:” the tendency of executives to

mindlessly imitate the behavior of their peers, no matter how

foolish it may be to do so. In their lending, many bankers

played follow-the-leader with lemming-like zeal; now they are

experiencing a lemming-like fate.

Because leverage of 20:1 magnifies the effects of managerial

strengths and weaknesses, we have no interest in purchasing

shares of a poorly-managed bank at a “cheap” price. Instead, our

only interest is in buying into well- managed banks at fair

prices.”

Thanks

LikeLike

Thanks for sharing 🙂 Investing in financial is basically a bet on integrity and competence of management team.

LikeLike

It seems that market is mispricing Yes bank “anticipating” that it is going the ICICI way on NPAs. If you look at last 8 year history, there were always fears of assets quality and till now it has come clean. Right now market is putting Kotak and IndusInd in the category of HDFC and YesB in the other category. If you look at history of Kotak/IndusIand, they were also not priced like HDFC few years back. Can Yes also come clean and join the HDF league ? Time will tell. Anyhow private banks have huge growth levers and the entire PSU space is up for grab in years to come.

RJ had recently mentioned that whatever ICICI’s sins are it was all the past boom lendings. Over the last few years, it has improved CASA, ROE and going the HDFC way. So I will watch out for ICICI also.

LikeLike

Yes, Although both IndusInd and Yes bank has very similar on Balance sheet size, Net Profits, ROA, ROE, NPA profile but IndusInd bank trades at twice the multiple of YES bank!!! Yes bank runs huge treasury operations (dunno why) and its loan book is predominated by corporate loan book. HDFC, Kotak, and IndusInd loan book is dominated by retail loans.One curious question to me: When the Indian corporates are under stress and all the PSU and private banks that funded them are showing NPAs. But how come Yes bank has very low NPAs? I can’t think of an answer.

I think women managers at top at both ICICI and Axis are doing fantastic job. After this NPA cycle, both will emerge stronger & other franchise like insurance, investment banking, asset management will also kick-in. Definitely investors should watch out.

LikeLike

Great analysis and thanks for sharing this

LikeLike

good post. saved a lot of number crunching.

LikeLike

Excellent analysis Eeswardev. Thanks much.

P.S. While reading your article it reminded me of Dr. Michael Burry (no pun intended)

LikeLike

Thanks for the kind words 🙂 am just starting the journey.

LikeLike

Interesting read, however, just wanted to know if there was any particular reason why J&K Bank has been included in the private sector bucket

LikeLiked by 2 people

Thanks 🙂 J&K bank is indeed an private sector bank as per its website and other sources. am i missing something?

LikeLike

It is a PSU bank! As per my limited knowledge. Great stuff here! Read both parts. Thanks for the post!!!

LikeLike

Pingback: Indian Banks – Part II | rberyblog

Brilliant analysis 🙂 Cuts through a lot of noise and focuses on what matters the most. Would look for forward to more insights from you..

LikeLike

Thanks for the kind words 🙂

LikeLike

Hi Jagdeesh,

I wanted to understand if (net NPA + net restructured loans) fully captures the loans falling under schemes like 5/25 and SDR. (This may be a very rookie question but I am not able to get my head around these terms).

Thanks,

Rohit

LikeLike

Hi Rohit, 5/25 and SDR are new tools that are made available to banks to tackle bad debt problems by RBI in this fiscal. All the numbers here are as of March 31, 2015 for the Annual reports. Need to wait for next i.e. FY’2016 annual report to see how banks classify them. Also remember these numbers do not factor in the stress in some of the heavily indebted corporates like ADAG reliance, GVK, GMR, Jaypee etc. They are paying interest so far and hence classified as standard assets. I expect more stress in these corporate loans going forward as they are struggling with poor cash flows from their big projects.

LikeLike

Thanks Jagadeesh 🙂

It will be interesting to look at FY15-16 ARs

LikeLike

Another great post!

LikeLike

Hi,

After your article, I have been trying to understand & analyze banking stocks. In view of this, could you please educate me on the term “Slippages”. Does this have to do with prior loans which were re-structured, again becoming NPA’s.

Also in ICICI results, ET in their articles mentions that “bank’s provisioning coverage ratio, computed in accordance with the RBI guidelines, was 53.2 per cent as of December 31, 2015”. What does provisioning coverage ratio mean.

Many Thanks

Nikhil

Source:

http://economictimes.indiatimes.com/articleshow/50757579.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

LikeLike

excellent view and analysis on bank please continue your writing

LikeLike

Pingback: Indian Financial Landscape through the eyes of Rashesh Shah (Edelweiss) | Ant Investor

Best article that makes sense on Indian Banking space

LikeLike

Excellent analysis ! I have just one question. Which is more risky to have deposits with PSU banks or to own shares of PSU banks ?

LikeLike

Thanks 🙂 Owning PSU banks is more risky due to equity dilution. All bank deposits (irrespective whether they are public or private) upto 1 lakh is insured by government. Government will never let them to go under. So no worries on deposits front.

LikeLike